AWS, Microsoft, Oracle, and Google Cloud Lead the Database Market, But AI Disruption Is Afoot

Gartner reports 'no churn' at the top, but new competitors are forging ahead.

Welcome to the Cloud Database Report. I’m John Foley, a long-time tech journalist who also worked in strategic comms at Oracle, IBM, and MongoDB. Connect with me on LinkedIn.

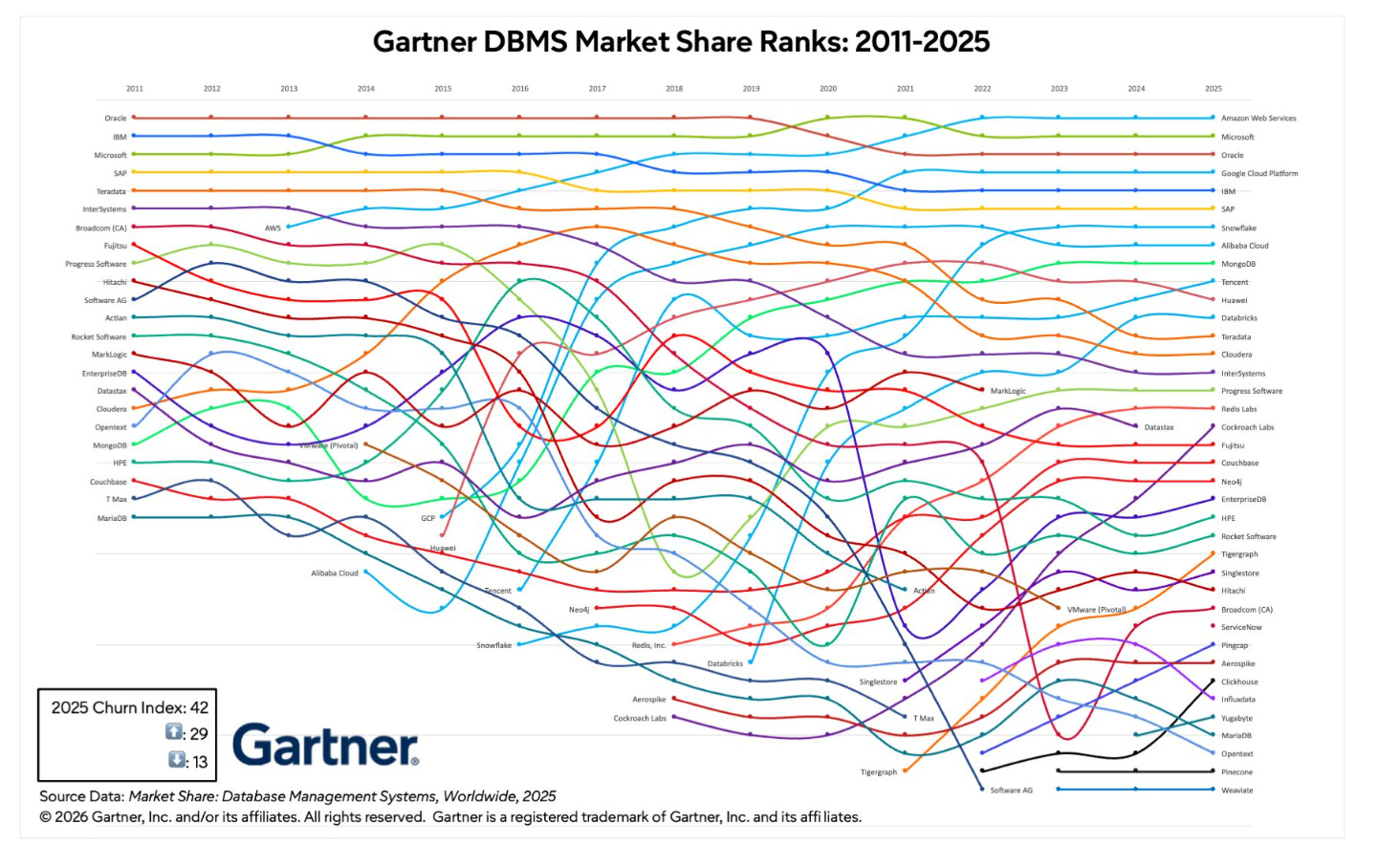

Gartner’s annual chart of database vendor revenues for 2025 shows a market that’s remarkably stable at the top — with no change whatsoever among the top nine database providers over the past three years.

In fact, there has been no churn among the top 17 vendors over the past 2 years, with one exception: Tencent passed Huawei. That insight is courtesy of Adam Ronthal, the Gartner VP who created and shared the awesome chart below along with some of his own valuable takeaways on LinkedIn.

If you focus only on the database leaders in recent years, it’s easy to conclude that the market is unwavering. But that’s not really the case. Under the surface, other players — Databricks, Cockroach Labs, Tigergraph, Clickhouse, and others — moved up in the ranking. And ServiceNow has been added to the mix.

What’s obvious at first glance is that the market leaders — AWS, Microsoft, Oracle, and Google Cloud, in that order — are unyielding fixtures, with no changes in their rankings over the past four years. But the waves of activity under the surface reveal that disruption is alive and well.

The churn is driven by AI and the rapidly changing nature of modern data management — data distribution, automation, multimodal data, reasoning, and hybrid transaction/analytical processing (HTAP). A few examples of the shifting paradigm, among many, include Snowflake’s data cloud, Databricks’ lakehouse, Cockroach Labs’ distributed architecture, and Salesforce’s zero-copy Data 360, each of which are representative of the changing landscape. On that point, Salesforce isn’t a cloud database vendor, per se, but its platform integrates, aggregates, analyzes, and shares data as if it were.

One thing that hasn’t changed: The 50-year-old relational database model is still going strong. Relational DBMSs, led by MySQL and PostgreSQL, are as popular as ever. Databricks and Snowflake last year added Postgres-compatible relational databases to their data architectures. See my post below for more on that.

Disruptive forces

Despite the locked-in status of the database leaders, major changes are afoot:

There’s tremendous development activity driven by AI and integration with LLMs. Legacy databases are being recast as AI databases.

There’s more data and new/emerging data types such as vectors, synthetic, audio, spatial, enumerated, and so on. Unstructured data is no longer locked up as PDFs, email, and media files. Databases are adapting to accommodate these new data types and/or special purpose databases like Pinecone and Weaviate (see chart) are springing up. Carnegie Mellon’s Database of Databases recorded 15 new databases in 2025.

Data architectures are increasingly decentralized, with data mesh, fabrics, data clouds, multi-cloud databases, edge devices, and more. Data sovereignty and resiliency requirements are forcing new thinking around how and where data gets stored.

Agentic AI and autonomous actions are game changers. AI agents must be able to tap myriad data sources (via MCP) in milliseconds. Those actions are based on the principles of learning and decision making via a reasoning engine. That’s the idea behind Google Cloud’s just announced Agentic Data Cloud, described as an AI-native architecture that evolves the enterprise data platform from “a static repository into a dynamic reasoning engine.”

Smaller fish, bigger pond

There’s little evidence that the Big 4 — AWS, Microsoft, Oracle, Google Cloud — are at risk of being displaced anytime soon. Each is doing its own version of the kinds of advances described above.

However, as the data and AI universe expands, the centralized databases of the Boomer generation are no longer the predominant model. Industry growth rates tell us that the database market is growing at a slower rate (↑13.2% to 16.5%) than AI in its various manifestations (global LLM market, ↑31.2% - 36.9%; global agentic AI market, ↑40.5% - 46.2 %; global GPU market, ↑30.2 % - 34.5%).

In other words, databases are becoming a smaller fish in a bigger AI pond, which helps explain the architectural shift underway.

Ephemeral databases

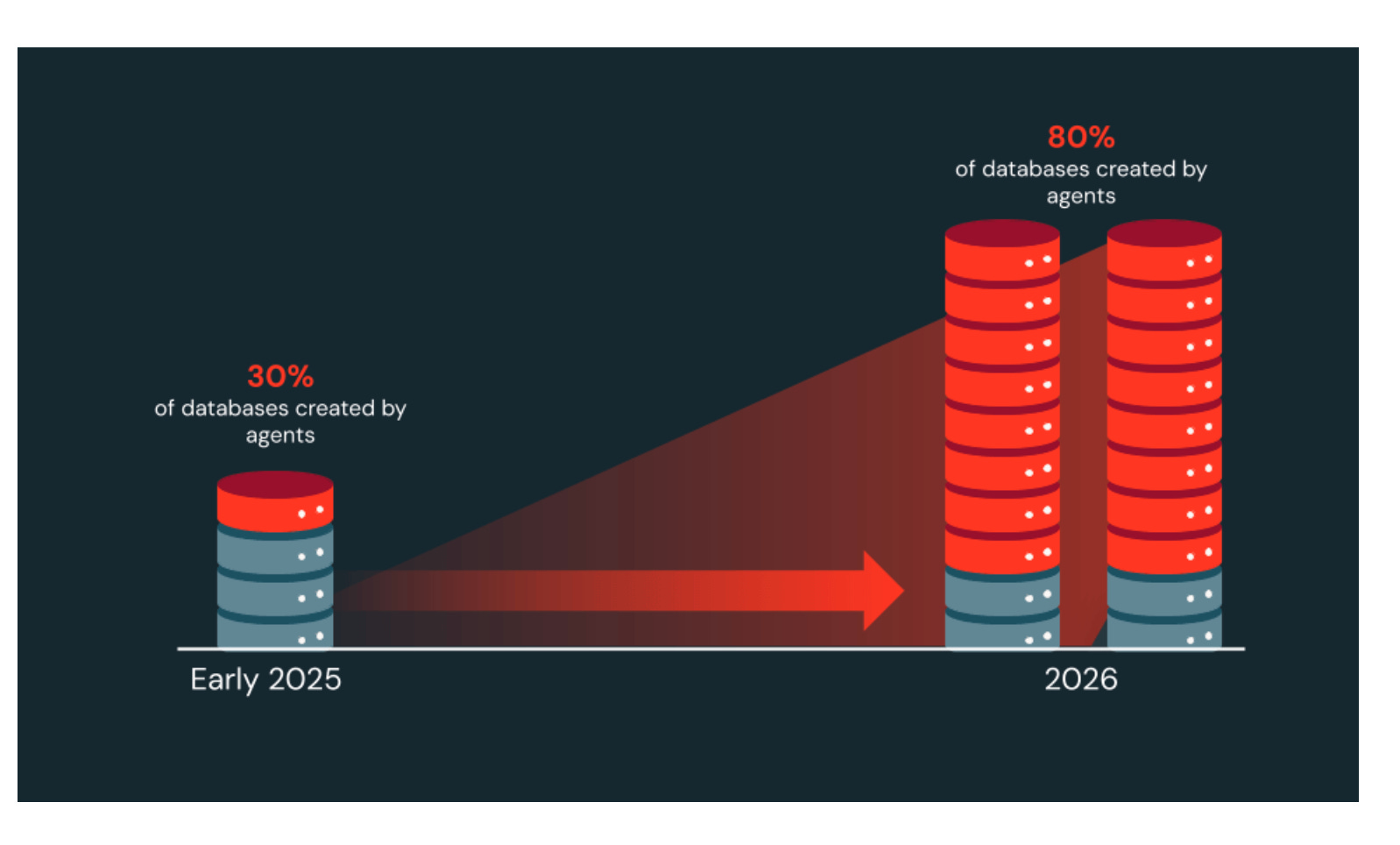

There’s something else at play. More databases are being created autonomously by AI agents, as you can see in the Databricks chart below.

As this happens, it points to a net increase in the sheer number of databases, driven by agentic AI. These are not the monolithic databases of the past; many are “small, ephemeral databases,” according to a Databricks post, “How agentic software development will change databases.”

“Our data shows that for about half of these agentic applications, the database compute lifetime is less than 10 seconds,” according to Databricks. “Traditional databases were designed as always-on infrastructure components with fixed provisioning and operational overhead. That model fits large, stable applications but fails economically when applications are numerous, ephemeral, and short-lived.”

Going forward, there will almost certainly be millions more databases deployed and in use. Today, Google Gemini says there are 29 million active enterprise-grade database instances supporting business operations. When you include small-footprint databases like SQLite on mobile devices and IoT, the number exceeds 1 trillion, per Gemini.

Note that Gartner’s market share chart is based on revenue, so pure-play open source databases aren’t represented beyond their commercial offerings.

Less is more

Data gravity is still very real — and helps explain why the market leaders are so hard to displace — but DBMSs are becoming less monolithic. Google Cloud describes its next-gen, cross-cloud, AI-native lakehouse as borderless. Cockroach Labs’ architecture has been called regionless.

So less is more in today’s database design.

Of course, we know that change is constant in the database market. Gartner’s spaghetti chart shows it’s been that way since 2011 — and well before, I would add. The market leaders may appear to be set in stone for now, but everything else is changing fast.